Unlike large caps, where it is difficult to add value and where passive strategies can provide an effective response, for small caps, active management offers a real opportunity to outperform the market by a wide margin. Not to mention its clear benefits in terms of responsible investment and shareholder advocacy.

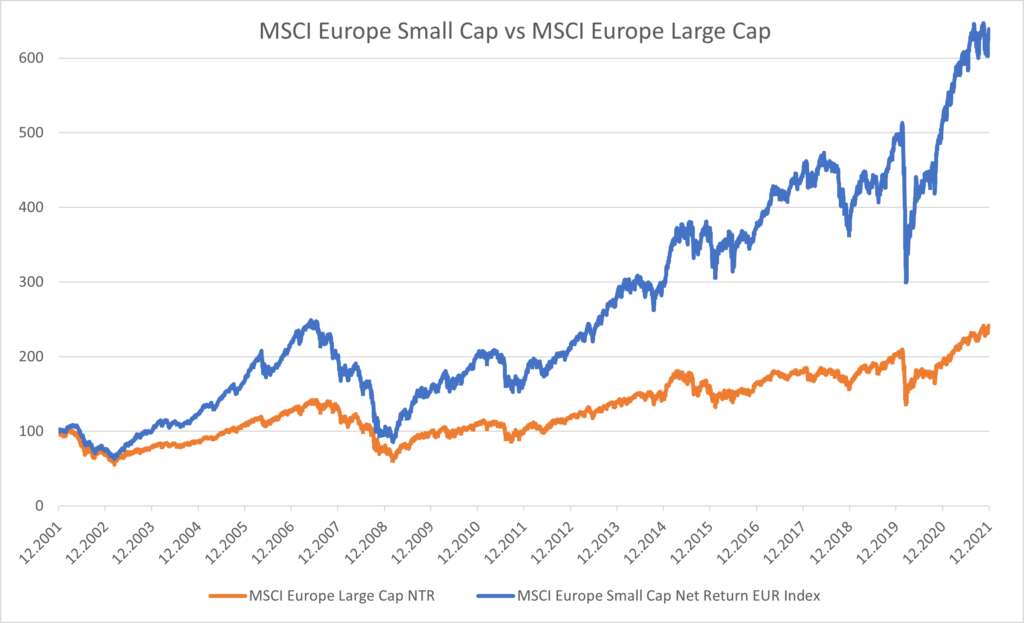

Small caps beat large caps…

Part of the reason for this is, of course, the so-called „small cap effect“, which allows smaller stocks to outperform larger companies over time. Indeed, when starting from a low level, it is naturally easier to achieve high growth rates than a company that is already mature, has already achieved a significant market share and is necessarily becoming heavier. Furthermore, stocks with a market capitalisation of less than one billion euros are often poorly researched and therefore poorly valued. Thus, in our Argonaut strategy, two-thirds of the companies in which we invest are followed by less than two analysts.

In concrete terms, as shown in the chart below, this translates into a large outperformance of small caps over 20 years in Europe compared to large caps (+494% vs. +141%).

And active management adds value

Given this lack of analysis and the potential for mispricing, management based on in-depth analysis of companies, both in terms of their financial situation, competitive position, products and management, can uncover undervalued stocks and thus outperform passive or index strategies.

This is especially the case as the size of the universe – over 7000 stocks in Europe – generally prevents passive funds or ETFs from gaining effective exposure or replicating the index, notably due to liquidity issues. Indeed, in our own management, trading in these types of stocks often requires contact with management and the use of highly specialised market intermediaries.

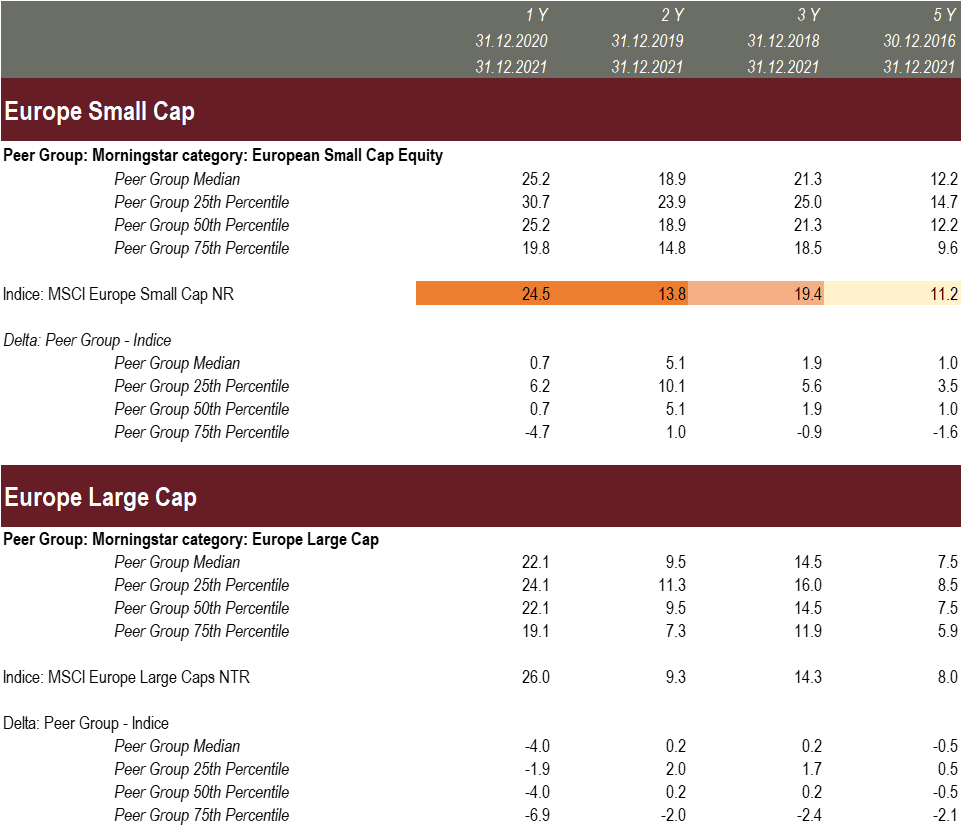

To verify this in practice, we selected a large peer group[1] of managers specialising in small and mid-caps from Morningstar and compared their results against the index over different periods.

As can be seen in the table above, the European small cap funds in the first two quartiles (i.e. the top 50%) have consistently outperformed the index over 1, 2, 3 and 5 years, with the median performance of the managers always higher. Only the managers in the bottom quartile did not generate alpha.

This is not the case for large caps. Indeed, while the best managers, those in the first quartile, have most of the time been able to generate alpha, those in the second, third and fourth quartiles have generally underperformed the indices. It is also worth noting that last year (2021), large cap managers in ALL quartiles underperformed the MSCI Europe Large Cap Index. The situation is very different in the small cap sector.

Passive management does not allow for responsible investing

Another important aspect is ESG. Indeed, a large majority of small and micro-cap companies are not rated by Sustainalitics, MSCI or other ESG rating companies. Passive investors are therefore „blind“ and will not be able to favour the „good“ companies or disfavour the „bad“ ones.

In contrast, at QUAERO CAPITAL, we systematically analyse all the companies in which we invest from an ESG point of view in order to form an opinion before making an investment. This allows us to effectively integrate sustainability criteria into our investment process.

Only active management can defend the interests of shareholders

Alpha generation also relies heavily on ‚engagement‘ with companies, through shareholder activism, to encourage them to adopt best practice and policies that benefit both shareholders and stakeholders. This ‚engagement‘ in key aspects of business strategy and ESG cannot be replicated in a passive approach. For example, in the case of a takeover bid, no analysis of the bid will be carried out and it will be automatically accepted.

Our recent success in obtaining higher prices in takeover situations illustrates this point. For example, a takeover bid was launched last year for one of our investments, the Dutch multinational Hunter Douglas. The majority family shareholder offered EUR 65 per share, a price that significantly undervalued the real value of the company. By aligning our position with that of other minority shareholders, we were able to resist and demand a higher price. A few months later, the offer price was raised to EUR 82, an already substantial +32% increase. At that point, we decided to double our position because it was clear that the majority shareholder would do everything to convince the remaining holdouts with more attractive offers, in order to achieve a squeeze out when the free float fell below 10%. At the end of last year, the family sold the company to a private equity firm for EUR 175 per share, 75% above the last quoted price and 70% above the level at which we doubled our position.

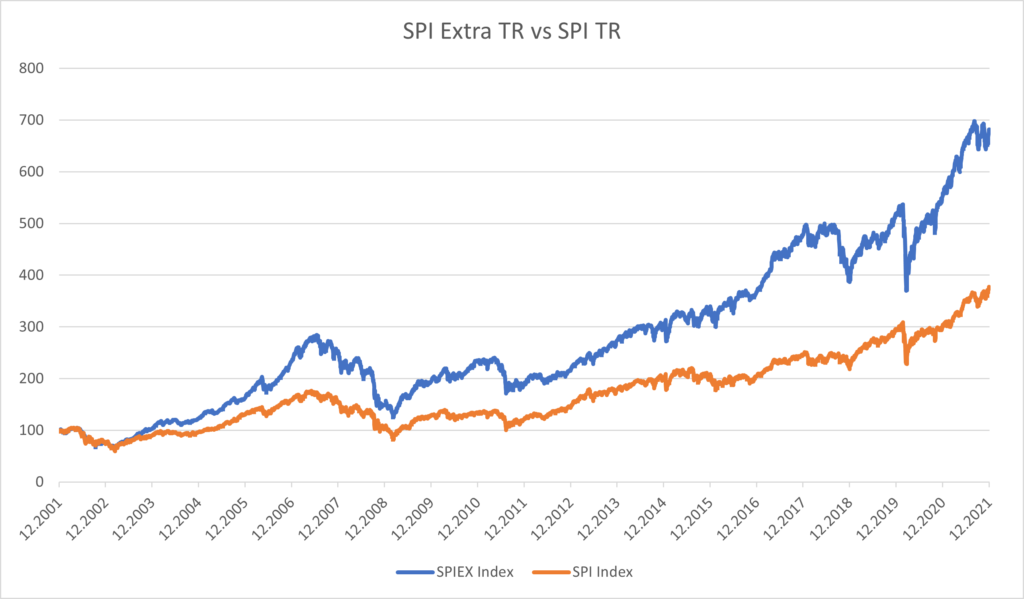

A similar situation in Switzerland

As can be seen below, the small cap effect is also true in Switzerland.

Indeed, with a performance of +581% over 20 years compared to +274%, small caps clearly outperformed the market leaders.

As regards active management, an analysis of the peer group[2] results leads to the same conclusions as for the European market: managers in the 1st, 2nd and 3rd quartiles generally outperformed the SPI Extra, with only managers in the 4th quartile lagging behind. This is not the case for Swiss large-cap funds: whether over periods of 1, 2, 3 or 5 years, only managers in the top quartile have managed to outperform the SPI.

Whether in Swiss or European small caps, there is thus a clear alpha generation by a wide range of managers, while this is not the case for large cap funds. Moreover, in small caps, only active management can effectively meet ethical investment criteria and truly defend the interests of shareholders.

[1] Morningstar Europe Small Cap Equity universe, funds > EUR 1 mn (129 finds), Morningstar Eurozone Large-Cap Equity, funds > EUR 1 mn (414 funds)

[2] Morningstar Switzerland Small/Mid-Cap Equity universe, funds > CHF 1 mn (66 funds), Morningstar Switzerland Equity, funds > CHF 1 mn (185 funds)