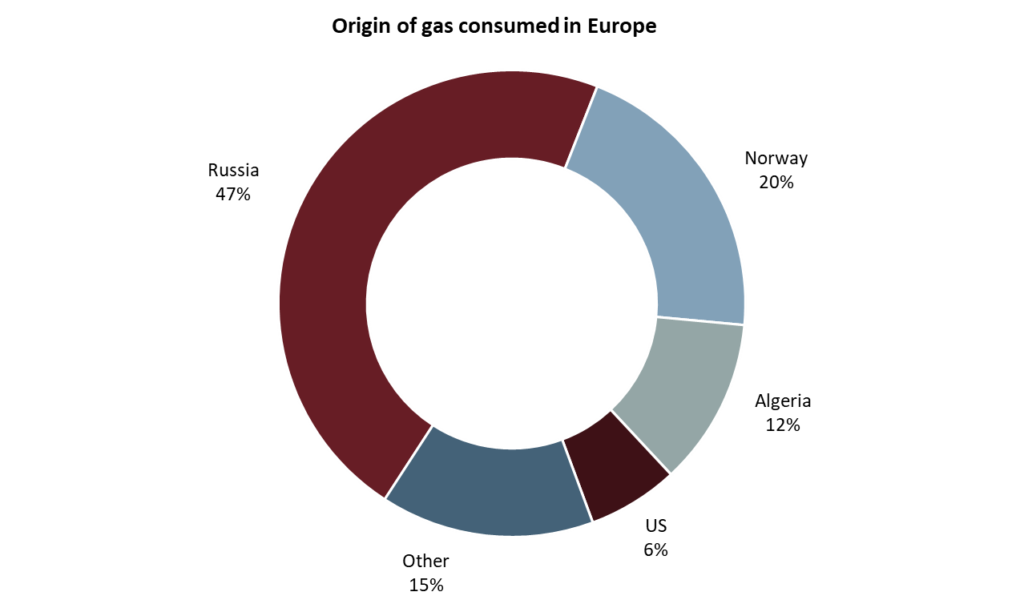

At present, the energy mix in the European Union is 42% fossil fuels, 35% renewable energies and 22% nuclear energy. And as the current crisis has unfortunately highlighted, most of the gas consumed in Europe comes from Russia (see graph below).

Source : Bruegel 2022 – Origin of gas consumed in Europe in 2021

The closure of the Russian tap has therefore led to major supply difficulties and a tenfold increase in the cost of electricity.

REPowerEu: a EUR 300 billion opportunity

As Churchill said, “Never let a crisis go to waste”. Europe has reacted by launching the REPowerEU plan, which, with a budget of EUR 300 billion, aims to transform the major problem of dependence on Russian gas into a unique opportunity through 3 major measures:

- Diversification into LNG and increased storage capacity. The EU is working with its international partners to find alternative sources of energy. In the short term, this means LNG, oil and coal, but in the longer term, the EU aims to develop green hydrogen.

- Energy savings of 9% to 13%, by raising awareness among citizens, businesses and organisations, but also by considering more restrictive measures.

- Acceleration of renewable energies from 35% to 45%. Indeed, in addition to its advantages in terms of CO2 emissions, renewable energy has become the cheapest and most readily available source of energy that can be produced locally. REPowerEU will accelerate its deployment and make massive investments.

Solar has a bright future

Depending on the energy source, the construction time for the different production infrastructures varies considerably. While it takes 10-15 years to build a nuclear power plant, it takes only 2-3 years for wind power, 2-3 years to build an LNG regasification facility, but only 6 months for a rooftop solar installation and 18 months for a photovoltaic park.

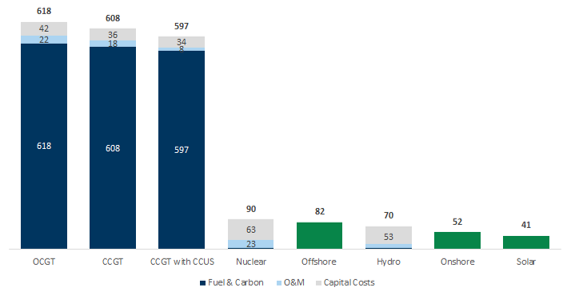

In terms of production cost, the advantage also lies with solar (see graph below – production costs are expressed in EUR/MWh).

Source: Eurostat 2021

The main obstacle to the development of solar remains the 2-3 year delays in obtaining permits, mainly due to appeals from local residents or associations, which are almost always rejected. REPowerEU therefore intends to encourage the states to limit these unnecessary appeals.

In 8 years, REPowerEU should allow a fourfold increase in solar production, from 150GW today to 320GW in 2025 and 600GW in 2030. In Switzerland, the installed capacity was 3 GW in 2021 and should reach 60GW in 2050 according to the Swiss energy strategy.

Equally strategic: reducing dependence on Asian semiconductors

Semiconductors are an essential element of the energy transition. They are used in the construction and implementation of all transition technologies. To produce 1 MW of solar energy, it is necessary to spend about EUR 3,000 on semiconductors, EUR 4,000 for 1 MW of wind power and EUR 1,500 to equip an electric vehicle[1].

However, 75% of these chips are manufactured in Asia, mainly in Taiwan and South Korea. This share even rises to 100% (92% Taiwan and 8% South Korea) for the latest generation of chips. The supply problems that arose with the COVID pandemic have raised awareness of this dependence and brought the issue of technological sovereignty back to the forefront. This resulted in major relocation plans, such as the CHIPS Act and the FABS Act in the USA or the European CHIPS Act in Europe.

Massive investment plans totalling USD 300 billion have been announced by major manufacturers such as TSMC, Samsung and Intel. In Europe, Intel plans to invest USD 20 billion in Ireland and USD 17 billion in Germany.

The growth prospects are therefore enormous for the semiconductor industry, whose turnover should leap from USD 600 billion in 2021 to USD 1,000 billion, or even USD 1,300 billion, by 2030, according to McKinsey.

Investment opportunity: the highly concentrated OEM market

Growth in the semiconductor industry means growth in the entire value chain. In particular, the fab equipment market is expected to grow from USD 90 billion in 2021 to USD 150 billion in 2030. In the three stages of deposition, lithography and etching, which account for 90% of the value, there are only a handful of players who will be the main beneficiaries of this race to independence.

[1] Sources : Shell 2021 and Infineon, August 2022.