The election of Joe Biden as the next President of the United States is a relief for those involved in sustainability. From an environmental perspective simply a return to science-based policy making will be hugely welcome. Biden plans to re-join the Paris Climate Agreement on day one of his presidency, and despite potentially not having control of the Senate he should be able to proceed with many of his green goals; a task force put together during the campaign identified 56 policy moves on climate and energy that do not need help from Congress.

There is of course another important factor in sustainability that has been highlighted by this election result, and that is the need for diversity. Kamala Harris is the first woman, and the first black or Asian American, to be vice-president-elect in the nation’s 244-year history, a hugely symbolic event during a period of heightened concerns regarding the slow global pace towards real diversity in politics and business.

The election of Kamala Harris is not the only bright spot. US politics has in fact become increasingly inclusive in recent years with the number of non-white US House and Senate members growing 84% in the last 20 years to represent 22% of all members. Considering 40% of the population in the US is non-white, however, there is some way to go. The fact that only 10% of non-white members of Congress are from the Republican party is notable. Women make up just over 50% of the population (women live longer than men which creates the imbalance) and yet hold just 25% of seats in Congress.

Source: Pew Research Center

While much progress has been made, there continues to be an underrepresentation of women and ethnic minorities in positions of influence across every country in the world, to varying degrees, and this goes beyond just politics. In the business world female CEOs lead just 5% of the FTSE100 index, 7% of Fortune 500 companies, 6% of the top 50 companies in Australia, 6% in China and one of the CAC 40 companies.

This lack of diversity matters to us as sustainable investors for two reasons. Firstly, gender equality and reduced inequalities are two of the 17 Sustainable Development Goals. Every person should be given equal opportunity and rights. It is a deeply complex discussion, and many questions remain as to whether women and people of diverse ethnicities are given equal opportunities. Whether due to active or subconscious biases, cultural impacts or the impact of unequal parental leave access, there are a multitude of biases and inequalities to help explain these figures. There are also fascinating studies that explore the reasons for these biases; scientists have shown that many of us harbour an implicit preference for our in-group (those like us) even when we show no outward or obvious signs of bias. These preferences can manifest in many ways; an often-quoted study at Columbia Business School took a Harvard Business School case study about a venture capitalist named Heidi Roizen and changed her name to Howard in half the classes taught. When the professors surveyed the students about their impressions about Heidi and Howard, while they were both rated as equally competent the students said they found Heidi less humble, more power hungry and self-promoting than Howard. These kinds of biases can prevent true equality of opportunity.

Secondly and importantly, diversity leads to financial success. McKinsey recently published a third edition of its study on diversity and financial performance demonstrating that diversity is key to financial success: Companies in the top quartile for gender diversity on executive teams were 25% more likely to have above average profitability than companies in the fourth quartile, and companies in the top quartile for ethnic diversity were 35% more likely to have above average profitability than those in the fourth quartile. Companies that pull back on diversity and inclusion, or fail to grasp the benefits, put themselves at a disadvantage by limiting their access to talent, diverse skills, leadership styles and perspectives.

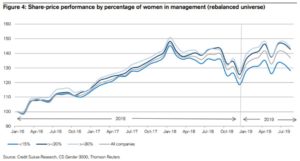

Credit Suisse published a similar report last year looking at gender specifically and found that there continues to be a performance difference between those companies that have greater gender diversity on boards and in management. The data is sector adjusted. The causality question remains; whether it is that more profitable companies are embracing diversity because they can afford to rather than diversity contributing to the probability of financial success. While bringing greater diversity into a team may require extra effort, it is unlikely to come at a great cost especially with continuing gender pay gaps. Conversely there are interesting studies and theories about how diversity actively benefits a company. Scott Page, a Social Science professor at the University of Michigan, wrote in his landmark book ‘The Difference’ that “when solving a problem, cognitive diversity can trump ability, and when making a prediction diversity matters as much as ability”. What we can at least conclude is that it is difficult to find statistical evidence that diversity reduces performance.

This issue is moving closer to the top of priorities for many asset managers. A group of asset managers, who between them manage €3trn in assets, have joined forces to demand that large public companies in France appoint more women to executive jobs. The group, which includes Amundi, Sycomore Asset Management and Mirova, announced this week that it is calling on the SBF120, the 120 largest companies in France, to hit a target of at least 30% women on their executive teams by 2025. Similar announcements were made earlier this year by Columbia Threadneedle and RBC Global Asset Management, who together manage nearly €1trn. These asset managers will vote against the Chair of the Nomination Committee where they do not see sufficient progress.

For us at Quaero Capital, we also that believe that diversity is important on boards and in management teams. We consider this not just on the basis of gender or ethnic background, but in cognitive diversity and diversity of experience. This forms an important part of our analysis of a company before investing, and we consider encouraging this part of our fiduciary duty and vote accordingly. We hope to see continued effort at company level across our investments to embrace the benefits of more diversity.

Important Information

The information contained herein is provided for discussion purposes only, is not complete and is not, and may not be relied on in any manner as, legal, tax or investment advice or as an offer to sell or a solicitation of an offer to purchase an interest in securities. QUAERO CAPITAL believes the information contained herein to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty is made, expressed or implied, with respect to the fairness, correctness, accuracy, reasonableness or completeness of the information and opinions.

The estimates, investment strategies, and views expressed herein are based upon current market conditions and/or data and information provided by third parties and are subject to change without notice. There is no obligation to update, modify or amend these materials or to otherwise notify a reader in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate.

These materials include certain opinions, statements and projections provided by Quaero capital with respect to the anticipated future performance of certain asset classes. Such opinions, statements and projections reflect significant assumptions and subjective judgments by QUAERO CAPITAL’s management concerning anticipated future events. these forward-looking statements are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond QUAERO CAPITAL’s control. In addition, these forward-looking statements are subject to assumptions with respect to future business strategies and decisions that are subject to change. The data as presented has not been reviewed or approved by any party other than QUAERO CAPITAL.

Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, currency rate or other market or economic measure.