With newspapers and inboxes dominated by COP26 news flow, we will wait until the two-week event is finished before we reflect on the many commitments, the potential disappointments and what impact it will all have. Instead, we are writing about gender diversity, a topic we have not touched on since the election of Joe Biden and Kamala Harris.

It was an important event for what it stood for, a symbolic election to put the first woman in the oval office. This was especially important in the middle of the Covid-19 pandemic, which had, and continues to have, a massive and disproportionate impact on women at work. As schools and childcare facilities closed, family support networks were off limits and families coped with an unfathomable change in lifestyle, many families were forced to make changes and more often this fell on women. According to a July report from the International Labour Organisation (ILO), 4.2% of women’s employment was lost during the pandemic vs. 3% for men. This was true throughout organisation levels, but especially apparent at senior level where the pressure to deliver at work and care for children at the same time pushed many women to step back.

Source: Women in the Workplace 2020 – McKinsey & Company and LeanIn

Gender diversity remains high on the sustainable agenda. Yesterday in France it was well publicised that for the rest of the year, women will be working for free, reflecting that the average wage for women is still 16.5% less than the average for men. As the momentum behind sustainability issues continues to power ahead, some governments have been responding with greater support for gender equality in the workforce.

Last week the French Senate approved text proposing the establishment of quotas for women in management positions of large companies. The quota will require any company with over 1,000 employees to have 30% or greater representation of women in their management teams by 2027, and 40% by 2030. Failure to comply with this rule will incur a fine of an amount up to 1% of total payroll. Currently women represent 25% of management committees of the 120 largest listed companies.

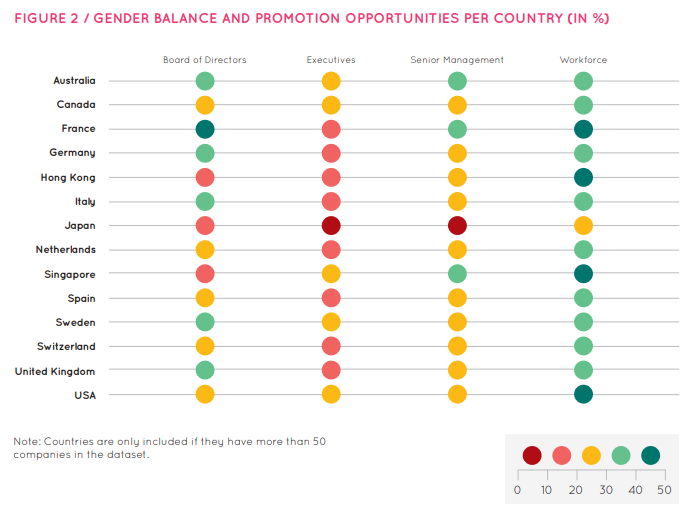

This bill arrives 10 years after the Cope-Zimmermann law, which set a quota of 40% of women on the board of directors of large companies by 2017, and three months after paid paternity leave was doubled to 28 days (it is mandatory to take at least one of the four weeks). According to Equileap, a provider of gender equality data and insights, France is now the best country for gender equality, closely followed by Spain and Sweden.

France is not the only country applying pressure on businesses to improve their diversity, however. The UK government is set to launch a new five-year push for more women on the boards of listed companies, setting fresh targets that at least 40% of every FTSE board should be female. It is also expected to focus more on encouraging female executives, where currently representation is poor in the FTSE 100 at just 14%.

The picture is less positive in Switzerland, which a recent report from Equileap highlighted appears to have a rather large glass ceiling – despite high representation of women in the workforce, few reach management, executive or board level. The Gender Intelligence Report from the University of St Gallen analysed 320,000 employees at 90 Swiss companies and found that only 17% of top management posts are held by women and 23% of middle management jobs.

Source: Equileap Global Report 2021

This momentum is seen not just in Europe but Asia and America too, although at a slower pace. We’ve seen stock exchanges announce plans to require progress from listed companies. Nasdaq stock exchange will require all listed companies to have one ‘diverse director’ by 2023, and two ‘diverse directors’ by 2025. The Hong Kong Stock Exchange, in an effort to attract foreign investment following Beijing’s takeover, proposed this summer to eliminate all-male company boards by 2025. This follows similar announcements from Malaysia and Singapore stock exchanges. In Japan, where gender diversity is poor, the 2021 updated to the Governance Code includes a requirement for disclosure of a policy and voluntary measurable targets with respect to promoting diversity in senior management, and a disclosure of HR development policies that ensure diversity.

The reality is that this push for greater gender diversity is coming not just from legislation but also from investors. Many large asset managers have committed to pushing companies for greater ethnic and gender diversity for their boards and workforces. BlackRock stated in their stewardship report in December 2020 that it would vote against directors who fail to act. It will require companies to disclose the racial, ethnic and gender makeup of their employees as well as the measures they’re taking to advance diversity and inclusion. Fidelity International, which manages $787bn in assets, has said it will now vote against directors whose boards fail to have at least 30% female membership in developed markets, and 15% in developing market. It has already started voting against all-male boards.

As sustainable investment becomes more embedded in the entire financial system, asset owners and managers are increasingly turning to engagement and voting to reflect a change at the heart of the industry, which is that as owners of companies we bear responsibility for the actions of the company; investment is no longer seen by many as investing in a paper asset but as being a business owner. Diversity, alongside climate risk management and environmental impact are high on those agendas; companies would be short-sighted to ignore these pressures for too long.